The Viral Claim

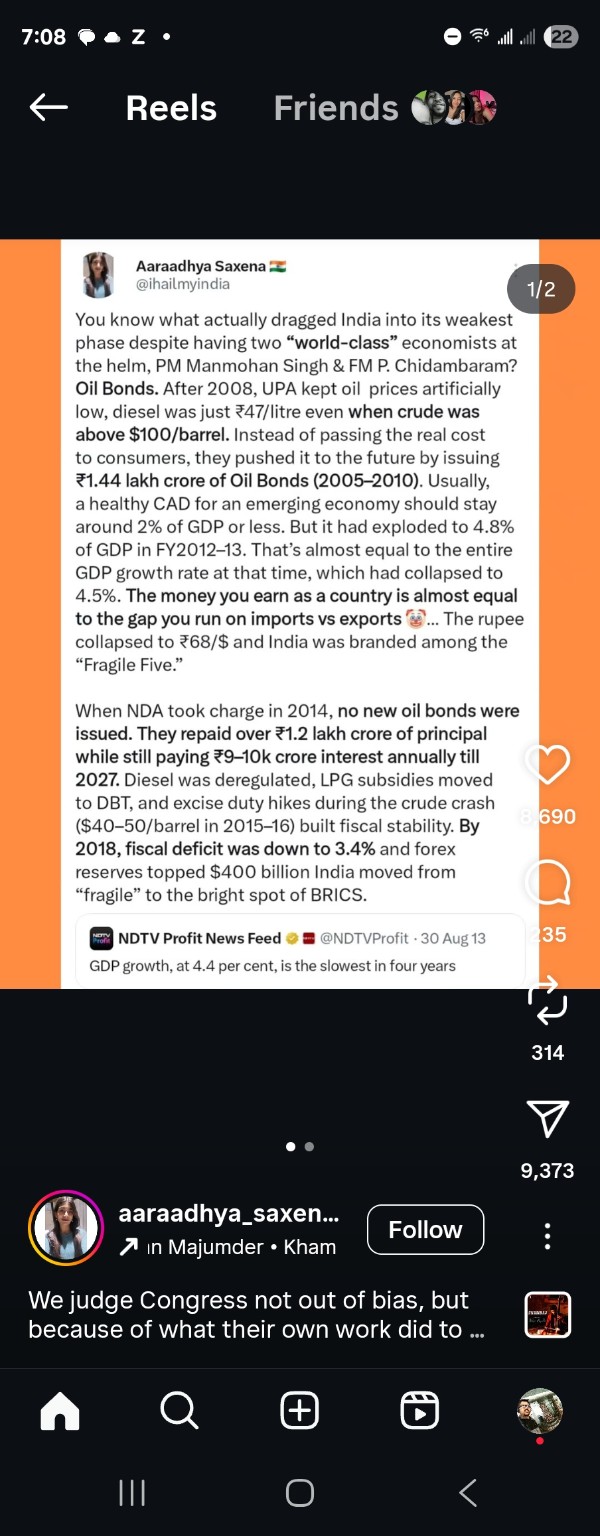

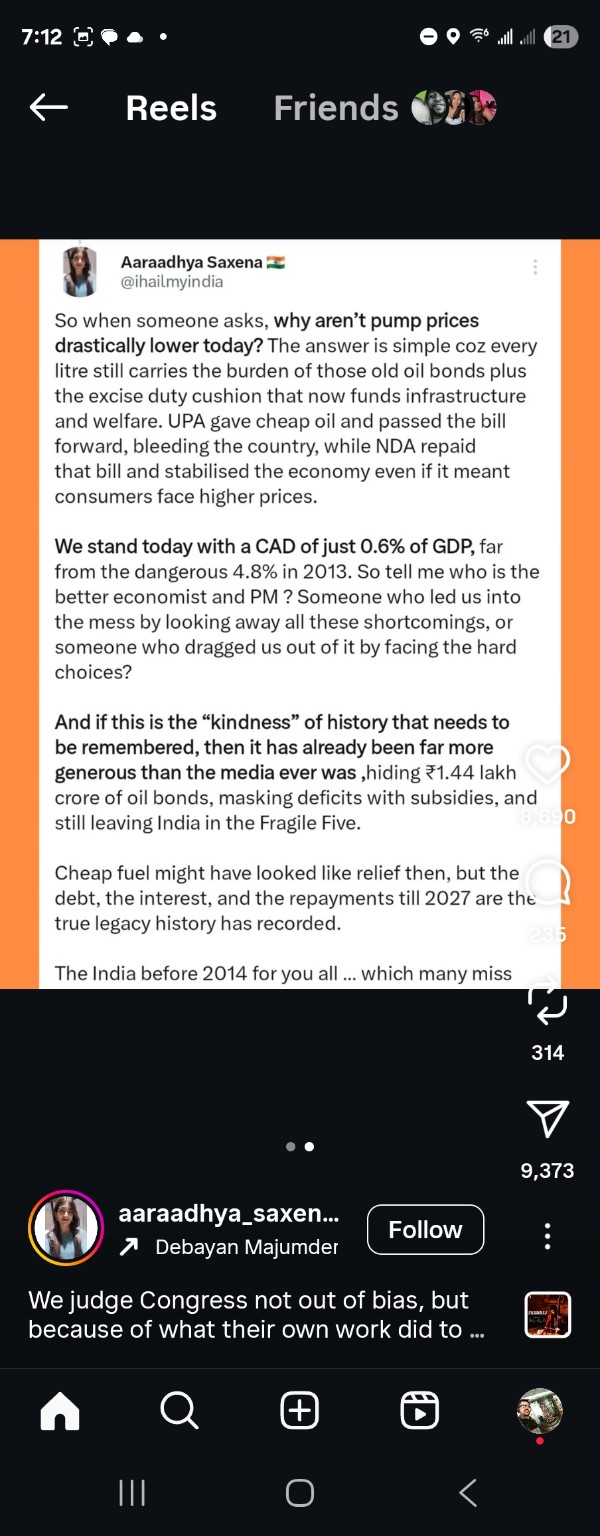

A widely shared social media post claims that UPA-era oil bonds worth ₹1.44 lakh crore are the primary reason for today’s high fuel prices, and that these bonds caused India’s “Fragile Five” status in 2013.

Our Rating: ❌ MISLEADING

While oil bonds exist and are being serviced, they represent only a tiny fraction of government petroleum revenues and cannot explain current high fuel prices.

📊 Research Foundation: ChatGPT Analysis

🔍 Evidence-Based Analysis

What Oil Bonds Actually Were

Oil bonds were special Government of India securities issued to state Oil Marketing Companies (IOC/BPCL/HPCL) in lieu of cash subsidy to compensate losses when retail prices were kept below cost price.

📋 Key Facts:

- Total Issued: ~₹1.34–1.44 lakh crore (face value)

- Period: 2005–2010 under UPA government

- Purpose: Off-budget financing to avoid showing higher fiscal deficit

- Interest Burden: ~₹9,000–10,000 crore annually

Source: CivilsDaily, Alt News

The Maturity Timeline

Official Government Data (Union Budget):

- Large chunks matured in 2021 & 2023

- A 2009 special bond series matures on February 4, 2026

- Most UPA-era bonds have already been repaid

Source: India Budget Receipt Budget 2025-26

💰 The Numbers That Matter

Annual Oil Bond Interest vs. Petroleum Tax Revenue

| Component | Amount (₹ Crore) | Percentage |

|---|---|---|

| Annual Oil Bond Interest | ~₹10,000 | 2.7% |

| Central Excise on Petroleum (FY2020-21) | ₹3,73,000 | 97.3% |

Reality Check: Oil bond servicing costs are less than 3% of what the government collects annually from petroleum taxes.

Source: Petroleum Planning & Analysis Cell

🏛️ Policy Changes After 2014

What Actually Changed

-

Diesel Deregulation (October 18-19, 2014)

- Cabinet decision to fully deregulate diesel prices

- Prices became market-determined

Source: Press Information Bureau

-

LPG Subsidy Reform (January 1, 2015)

- PAHAL/DBTL scheme nationwide rollout

- Direct transfers reduced leakage

Source: Press Information Bureau

-

Excise Duty Strategy

- Centre raised excise multiple times during 2014-16 crude crash

- Captured crude windfall as tax revenue instead of passing savings to consumers

The Global Oil Price Context

Crucial Timeline:

- 2014: Oil >$100/barrel

- 2015-16: Crashed to $30-40/barrel

- Late 2016: OPEC cuts began recovery

This external tailwind materially eased India’s Current Account Deficit and inflation pressures.

Source: Macrotrends Oil Price History

📉 The “Fragile Five” Story

What Really Happened in 2013

India’s Current Account Deficit Crisis:

- Peak CAD: 4.8% of GDP in FY2012-13

- Causes: High oil & gold imports + US taper tantrum

- External factors: Global capital flow volatility

Source: Times of India

Post-2014 Improvement:

- CAD fell to ~1-2% of GDP

- Primary driver: Global crude price collapse, not just oil bond policy

- Recent data shows CAD remains manageable

Source: Reuters on India’s Current Account

🎯 Claim-by-Claim Verification

”NDA Repaid ₹1.2 Lakh Crore”

What Officials Say:

- Ministers stated ~₹1.5 lakh crore UPA-era bonds remained as of 2021

- Significant maturities occurred in 2021 & 2023

- Verdict: Partly accurate on repayments, but exact figures not verified in official records

Source: NDTV Report

”Interest Payments Continue Till 2027”

Official Maturity Schedule:

- 2026 is the documented final maturity date

- “Till 2027” claim not supported by government bond records

- Verdict: Timeline exaggerated

📊 Evidence Scoreboard

| Claim | Evidence Level | Verdict |

|---|---|---|

| Total bonds ~₹1.34-1.44L cr | Strong (Multiple sources) | ✅ TRUE |

| Annual interest ~₹9-10K cr | Strong (Budget data) | ✅ TRUE |

| Bonds keep prices high today | Weak (Data shows <3% impact) | ❌ MISLEADING |

| Caused 2013 “Fragile Five” | Weak (Multiple macro factors) | ❌ OVERSTATED |

| NDA repaid ₹1.2L cr exactly | Unverified (No official breakdown) | ⚠️ PARTLY ACCURATE |

🔍 What The Data Actually Shows

1. Scale Reality Check

- Oil bonds are a minor fiscal burden compared to petroleum sector revenues

- Current high prices driven by excise policy and crude cycles, not legacy bonds

2. Policy Trade-offs

- UPA: Consumer relief via off-budget financing

- NDA: Fiscal revenue maximization via high excise duties

3. Global Context Dominates

The 2014-16 crude collapse was the primary driver of India’s improved macro metrics, not just domestic oil bond policy.

⚖️ Third Angle Assessment

What’s True:

- UPA issued ~₹1.4L crore oil bonds (2005-2010)

- NDA stopped issuing new bonds and serviced existing ones

- CAD improved dramatically from 2013 highs

- Diesel was deregulated and LPG moved to direct transfers

What’s Misleading:

- Oil bonds are the primary reason for high fuel prices today

- Bond repayments alone stabilized India’s macroeconomy

- India’s 2013 crisis was caused by oil bonds specifically

The Real Drivers:

- Excise duty policy (₹3+ lakh crore annually)

- Global crude price dynamics

- Currency fluctuations and import costs

🎯 Bottom Line

Oil bonds are real and represent a fiscal legacy, but they’re not the villain in today’s fuel price story. The real debate should focus on:

- Tax policy transparency

- Balancing consumer relief vs. fiscal health

- Managing external oil price shocks

Both UPA and NDA made policy choices with trade-offs. Understanding these nuances matters more than partisan blame games.

📚 Comprehensive Sources

Government & Official Data

- India Budget Receipt Budget 2025-26

- Petroleum Planning & Analysis Cell - Tax Revenue

- PIB - Diesel Deregulation

- PIB - LPG PAHAL Scheme

Independent Fact-Checks

- Alt News - Oil Bonds Analysis

- Moneycontrol - Interest Payments Fact-Check

- CivilsDaily - What are Oil Bonds

Economic Data

- Macrotrends - Crude Oil Price History

- Times of India - CAD Record High

- Reuters - India’s Current Account Data

- NDTV - Oil Bonds Repayment

- Indian Express - CAD Crisis Analysis

This comprehensive fact-check was conducted using official government data, budget documents, RBI reports, and cross-verified through multiple independent sources. Third Angle maintains strict editorial independence and presents evidence-based analysis without political bias.

Share this research to promote informed debate on energy policy

#OilBondsFactCheck #EnergyPolicy #DataDrivenAnalysis #ThirdAngle